Burn the Mortgage!

Burn the Mortgage – Paydown Progress

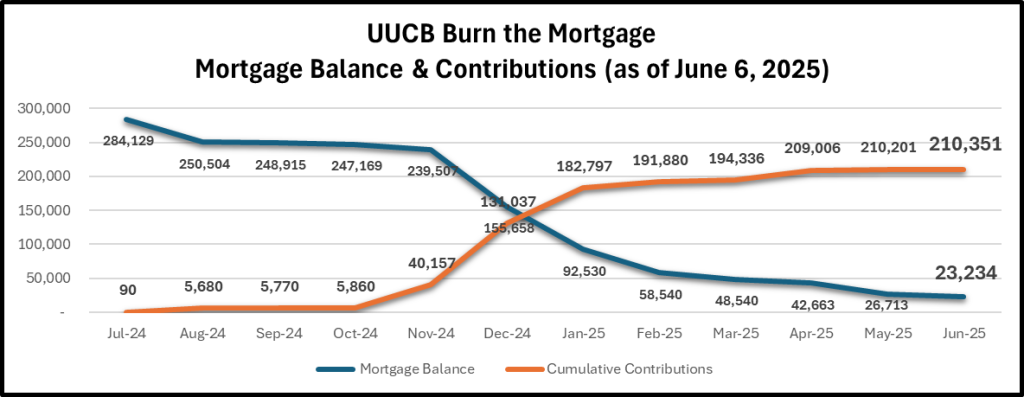

As of June 6, 2025, the Burn the Mortgage campaign has received $210,201 in contributions that have all been applied to the mortgage balance. Our Visions Loan balance stands at $23,234. In addition to the donations from congregants, we have made our monthly payments as well as applied an UUCB Endowment grant of $6,185. Let’s keep up the momentum!

The Simple Facts:

- The current mortgage payment is a burden on our annual budget ($29,000 per year – 8% of Budget)

- The interest rate will go up significantly in a year, leaving us with a large balloon payment in 2035.

- We can do this! Over the next 12 months, we need to raise $232,000 (the amount that will be left in Nov. 2025)

Background:

Renovation

* In 2020, UUCB undertook an ambitious building renovation.

* Raised over $1.6 million to complete the project between cash, grants, and loans.

* Loans include $400,000 from Visions and $100,000 from the UUCB Endowment Fund.

* Moved back into the building in 2021.

* Working to put on the finishing touches now: acoustic panels in Social Hall and insulation in the attic.

Visions Loan

* Borrowed $400,000 from Visions in total, due in full in 2035.

* Monthly payments do not change.

* Interest rate will change Nov. 2025 from 4% to likely 10%+ (the prime rate +3%).

* As of Oct. 2024, have $250,000 left on the Visions Loan.

Impact on Annual Budget

* Annual repayment is $29,087, or $2,423.92 per month.

* The loan payments account for 8% of UUCB’s annual budget.

* Early pay off will reduce this added burden for operating costs.

Impact on Total Interest Paid

* Early pay off will save UUCB just shy of $200,000 over the life of the loan, assuming the interest rate does not decrease in 2030.

Burn the Mortgage Spotlight:

Pay Off Scenarios:

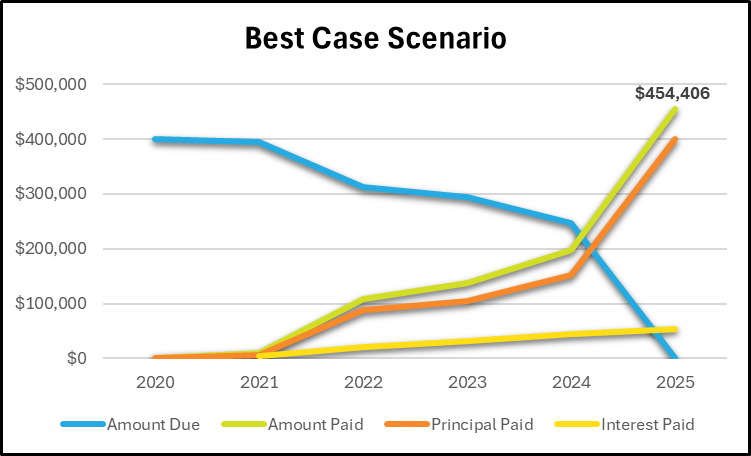

Under the Best Case Scenario, UUCB raises $225,000 by November 2025 and can pay off the loan in full. In this scenario, UUCB would ease the burden on the Annual Budget before the interest rate increases.

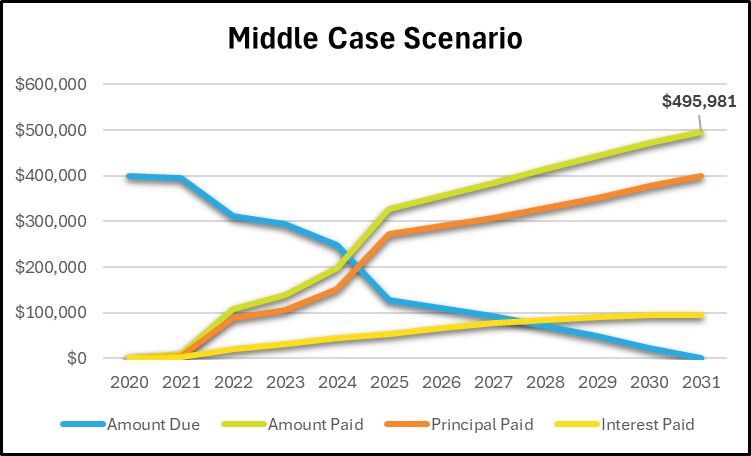

The Middle Case scenario portrays UUCB raising an additional $100,000 to pay down the principal of the loan. Assuming stable interest rates in 2030, UUCB would be able to pay off the loan in full in 2031. The middle scenario would result in an additional $50,000 in interest over the life of the loan over the best case scenario.

Translation: It is worth pursuing, even if we are unable to reach our final goal!

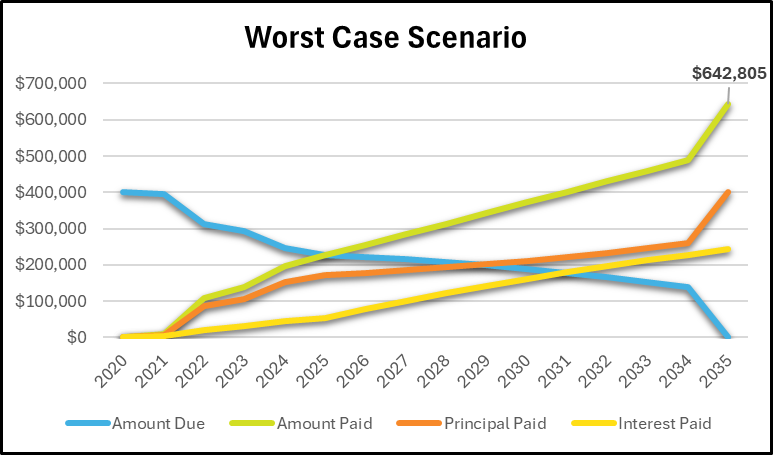

The Worst Case Scenario is one in which the congregation makes no additional payments toward the principal. Assuming stable interest rates in 2030, UUCB would have a balloon payment of approximately $125,000 in 2035. The Worst Case scenario would also result in almost $200,000 more paid in interest over the best case scenario.

Making a Pledge:

Ready to make a donation or a pledge?

Donate link is at the top of the page. Checks or cash can be deposited in the collection plate or the safe in the office. Please indicate “Burn the Mortgage” on the memo line or envelope.

Pledges let us know how much you intend to give, even if you are not able to do so today.

https://onrealm.org/UUCB/give/burnthemortgage

Need guidance on how much to give?

- First and foremost, only give what feels comfortable to you.

- Ask friends & family to consider contributing on Giving Tuesday, Dec. 4th, or gifts for birthdays & other special occasions.

- See the Creative Giving section for some ideas.

Creative Giving:

- Qualified Charitable Distribution (QCD) – QCDs are a major source of funds for congregations. People aged 70 1⁄2 or older are eligible to transfer up to$100,000 tax-free each year from their IRA to eligible charities, including this Burn the Mortgage campaign. And QCDs count toward your Required Minimum Distribution!

- Canceling Subscriptions – How many streaming services subscriptions do you have? Do you use all of them/get your money’s worth? Consider finding one that you can give up for a year and set up a recurring donation of that amount to UUCB.

- Remodeling – Sue and Jim had saved $500 a month for the past five years to remodel their kitchen. It occurred to them that if they could save $500 a month for the past few years, why not defer the kitchen project, give the saved amount — $30,000 — to the campaign, and start saving now once again for the kitchen. They realized they could do the kitchen any time but contribute to this campaign only now.

- Advance on Inheritance – a young couple surprised the visiting steward by making a $25,000 gift to the capital campaign. They told the steward that at first they were unhappy with how little they could contribute having few assets and already being generous givers to the annual fund. When they learned that for a $25,000 gift they could name a room in memory or honor of someone, they really wanted to do that for the mom of one member of the couple who had died suddenly the year before. So they approached the surviving dad and suggested taking an advance on their inheritance – a request joyfully answered in the affirmative.

- Tithing based on Assets – A member of a congregation in the West indicated his intention to give 10% of his assets. And while not everyone is in a position to tithe, thinking about a percentage of assets can be a useful way to think about a Burn the Mortgage contribution.

- Shifting Funds from Estate Plans – People who have included the congregation in their estate plans might consider giving some or all of that money now instead. Why not see the money put to concrete use to give a significant boost to the Burn the Mortgage campaign rather than letting the opportunity pass by?

More Questions?

Reach out to a member of the Burn the Mortgage team: Kathleen McKenna, Eric Cotts, Gay Canough, and Emily Hotchkiss-Plowe.